As 2025 closed, Dubai’s real estate market remained exceptionally active, but with clear signs that the pace of growth is shifting into a more balanced and sustainable phase. While transaction volumes stayed at historic highs and off-plan activity strengthened, pricing eased slightly and buyer behaviour became more selective - a natural progression for a market that has expanded at record speed over the past few years.

Prices Ease Slightly, But Long-Term Growth Remains Strong

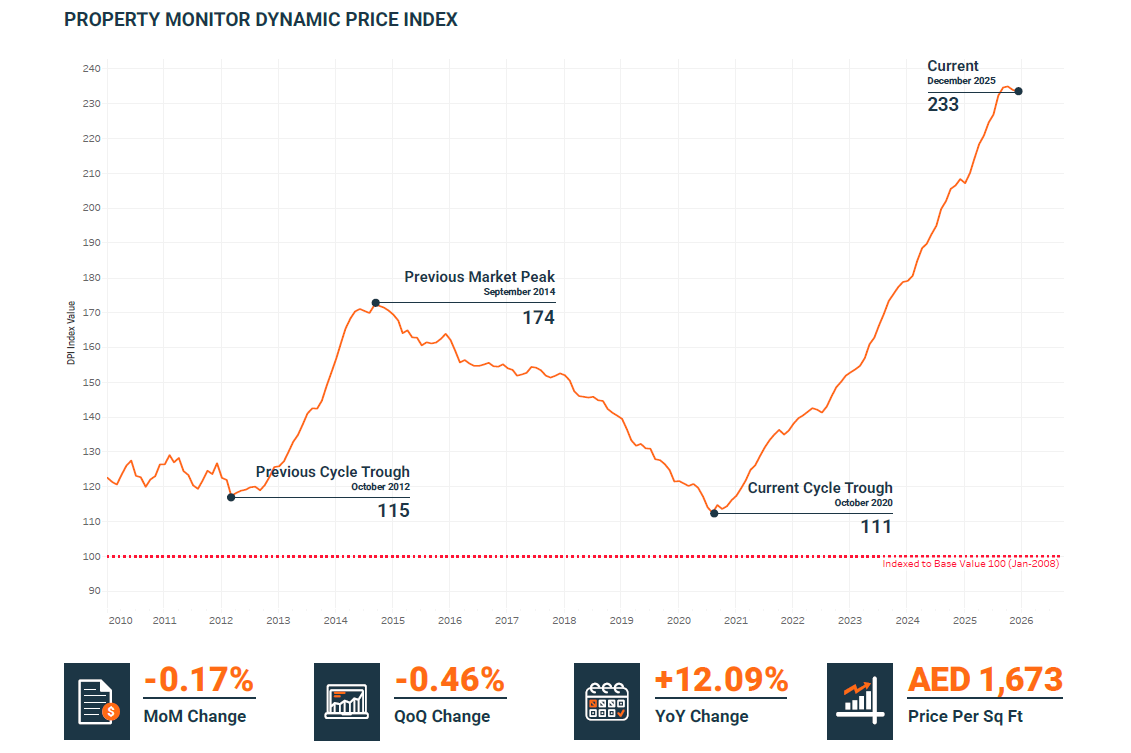

In December, property prices softened marginally for the second month in a row, with the Dynamic Price Index recording a 0.17% month-on-month decline, following a 0.42% dip in November.

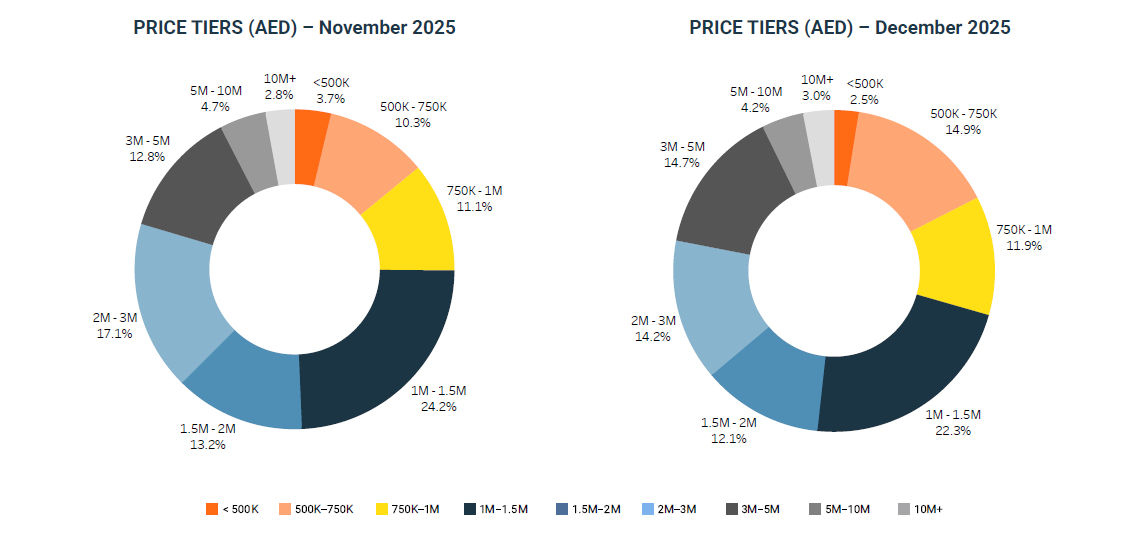

Average prices now stand at approximately AED 1,673 per sq ft, which still places the market:

- Over 35% above the previous peak in 2014

- More than double the price levels seen at the 2020 market low

Rather than indicating weakness, this modest adjustment reflects a period of price consolidation, where values stabilise after several years of rapid growth. The market is not reversing - it is recalibrating.

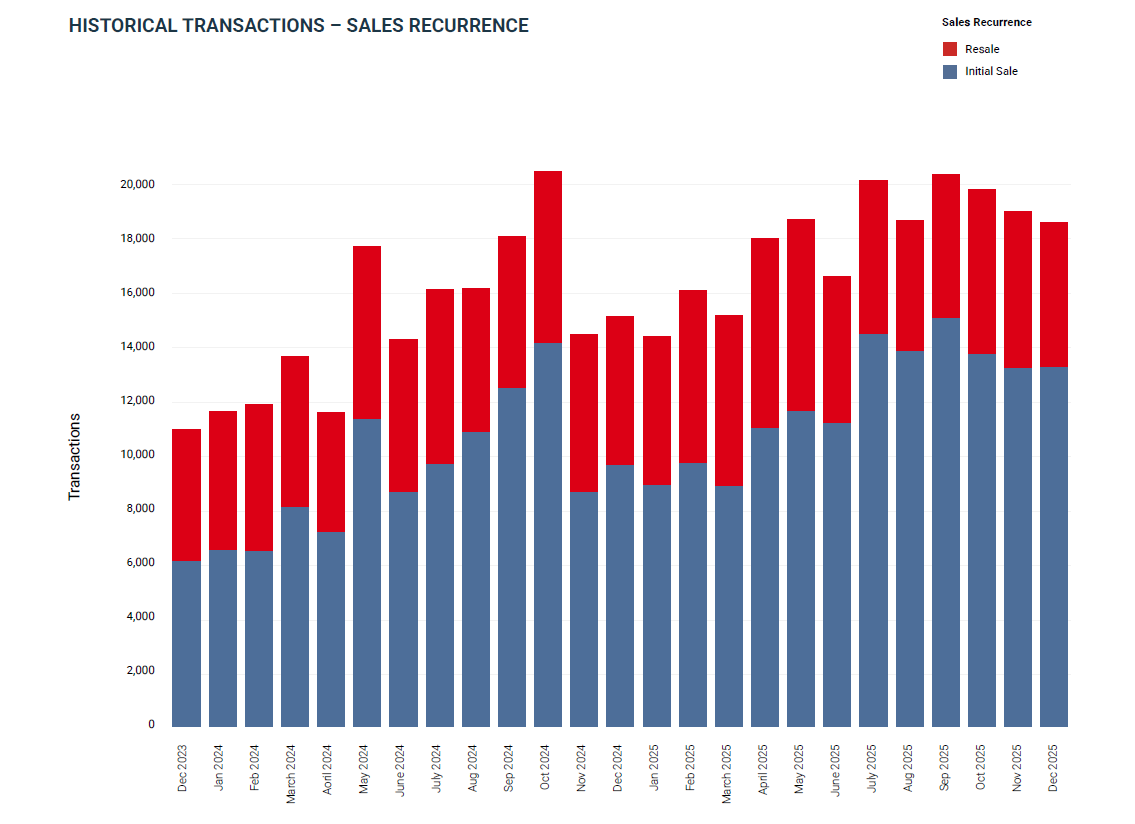

December Ends as the Strongest on Record for Sales

Despite a slight slowdown compared to November, 18,575 transactions were recorded in December, making it the strongest December ever for Dubai real estate.

Looking at the full year:

- Total 2025 transactions reached 215,458, representing an 18.9% increase over 2024

- Residential properties continued to dominate, accounting for almost 94% of all transactions

- Apartment and villa sales led growth, both increasing by over 20% year-on-year

This confirms that buyer demand remains deep and broad-based, even as pricing and supply dynamics evolve.

Off-Plan Strengthens Further into Year-End

Off-plan sales regained momentum in December, with 13,039 Oqood transactions, lifting the off-plan share to:

- 70.2% of all sales officially, and

- 73.3% when adjusting for registration technicalities

This reinforces that new developments remain the primary driver of transaction volumes, supported by:

- Continuous project launches

- Developer incentives and extended payment plans

- Strong investor appetite for under-construction stock

Meanwhile, completed property transactions continued to soften slightly as buyers weighed value more carefully against developer offerings.

Resale Activity Moderates as Holding Periods Extend

Resale transactions fell to 5,233 sales, making up 28.2% of total market activity.

While off-plan resales ticked up slightly month-on-month, the 12-month rolling average continued to decline, pointing to:

- Fewer short-term exits

- Longer holding strategies among investors

- Reduced speculative flipping compared to earlier stages of the cycle

This is another signal that the market is becoming more mature, with buyers increasingly focused on medium- to long-term value rather than rapid resales.

New Supply Reaches Historic Levels

Development activity in 2025 was unprecedented:

- Over 167,000 units launched during the year

- Across 648 new projects

- Representing approximately AED 463 billion in potential sales value

- Equivalent to a new project launch every 13.5 hours

In December alone:

- 37 projects were launched

- Delivering over 10,000 new residential units worth AED 30.2 billion

Apartments dominated supply by volume, while villas and townhouses - though fewer in number = represented a much higher share of total value, reflecting continued demand for premium, lower-density homes.

While developer confidence remains strong, the growing pipeline places greater emphasis on absorption rates, product differentiation, and realistic pricing strategies moving forward.

Mortgage Activity Declines, Driven by Sales Mix

Mortgage registrations fell sharply in December to 3,612 loans, a 19.8% month-on-month decrease. However, this appears to be driven more by the type of properties selling rather than tighter lending conditions.

Key trends include:

- Over 51% of loans used for new purchases

- Average mortgage size around AED 1.83 million

- Loan-to-value ratios holding near 73%

- Growth in refinancing and equity release activity

With villa demand remaining relatively steady and apartment transactions softening slightly, mortgage volumes reflect changing buyer preferences rather than reduced access to finance.

What This Means for 2026

Dubai’s real estate market is entering a phase where:

- Growth continues, but at a more measured pace

- Buyers are more price-sensitive and value-driven

- Developers must compete more on product quality, design, and delivery timelines

Population growth, economic strength, and Dubai’s global positioning continue to provide solid long-term fundamentals. However, the next stage of the cycle will be shaped less by how fast new projects launch and more by how effectively they are absorbed by the market.

Our View at Exclusive Links

From our perspective, this transition is a positive and necessary evolution. A market driven by informed buyers and sustainable pricing creates healthier long-term outcomes for homeowners and investors alike.

Whether purchasing off-plan, upgrading to a villa, or building an investment portfolio, strategy now matters more than speed and expert guidance plays a critical role in navigating this increasingly competitive landscape.

Market Data Credit

This article is based on data and insights from the Property Monitor December 2025 Report. Property Monitor is the UAE’s leading real estate intelligence platform, providing transparent, RICS-accredited market analytics and transaction data trusted by developers, banks, government bodies, and property professionals across Dubai. The above reflects a summarised interpretation of their published findings.

Are you looking for a name you can trust?

We harness professional and market expertise from all areas of the business and work with a transparent client centric approach.